When Google made Hosted Card Emulation (HCE) available for its mobile payment in order to bypass telecoms’ control, the debate of HCE and Secure Element (SE) continues.

A webinar “Evaluating NFC security strategies: The role of the secure element in the evolving landscape” was hosted by NFC World on January 20, 2015.

A few highlights of the webinar is as follows:

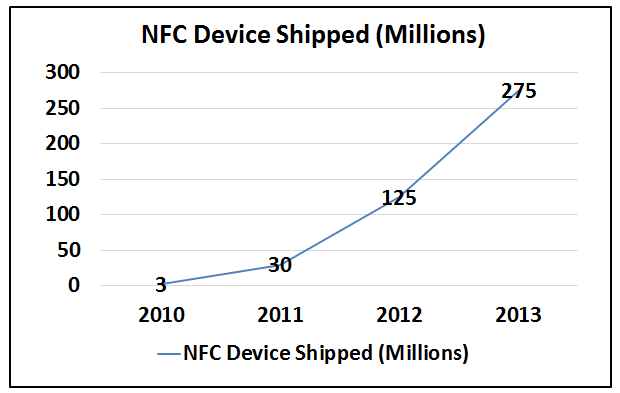

- The NFC adoption rate is increasing rapidly based on the stats of NFC SIM shipped; 16M shipped in 2011, 30M in 2012, and 72M in 2013.

- Geographic stats show the demand in different regions. In 2013, 37M was shipped to Japan/Korea, 24M to North America and 14M to Europe.

- The pros and cons analysis of HCE and SE technology.

- A SIMalliance recommended deployment model based on security and market reach, application and technology requirements.

- A case study on Canada’s success as the #1 mobile payment country in the world. Some stats are as follows: All of Canada’s major MNOs now offer SE based NFC payment capability to their customer; 2/3 of the phones are Android and BlackBerry; 5 of Canada’s “Big Six” Financial Institutions do the same; over 84% major retail merchants have contactless EMV terminals

SIMalliance anticipates a future where SE and HCE will continue to co-exist and in many cases converge. This will be the basis of an optimally efficient and secure NFC ecosystem.

To watch the free seminar, click the link.

![IMG_0321[1]](http://everydaynfc.files.wordpress.com/2014/04/img_03211.jpg)